Q3 2021 = Q1 + Q2 +Q3 + Q4 2020

With $817m+ raised in September alone, start-ups in Africa keep setting the bar higher and higher

As we enter Q4 , we thought it was a good opportunity to take stock of an incredible 2021 so far in terms of fundraising:

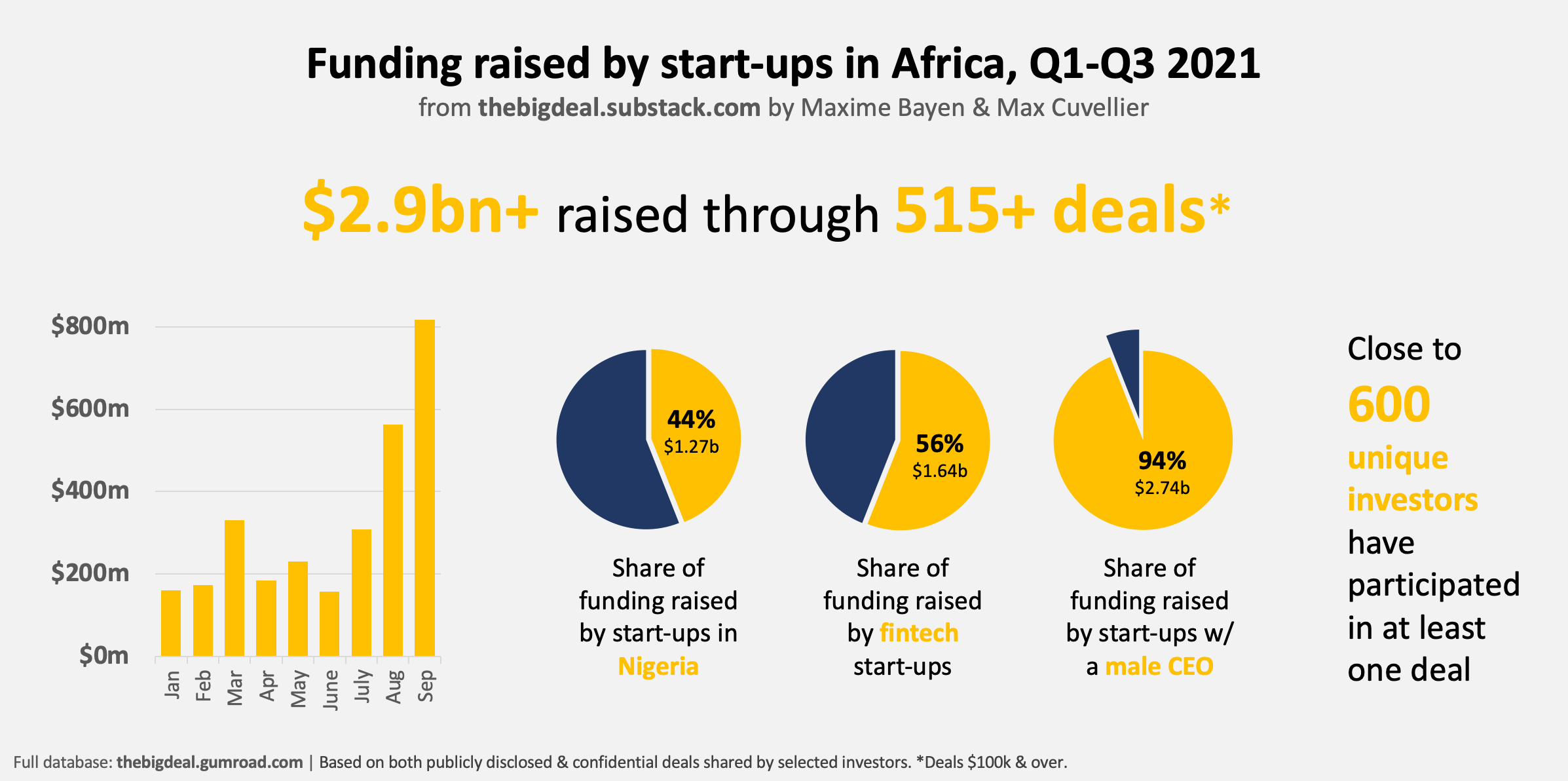

How much? Since the beginning of the year, start-ups in Africa have raised more than $2.9bn through 515+ deals $100k & over (about 200 of these deals were $1m & over). If we take into account deals flying under the radar, and the Swvl transaction which will only be effective in November, we can consider that the $3bn milestone has now virtually been reached.

When? The past two months (August & September) have seen extraordinary levels of activity, and represent almost half of the funding raised in Africa this year so far (47%, $1.4bn). More has been raised in those two months than in the whole of 2019. The amount raised in Q3 2021 is equivalent to the full amount raised in 2020.

Where? Nigeria represents 44% of the total funding raised in 2021 to date ($1.27b), followed by South Africa ($481m, 16%) and Egypt ($434m, 15%). The remaining 25% ($733m) is shared between the other 23 countries where at least one $100k+ deal has occurred this year. It also means 28 countries have registered no significant public VC activity this year so far.

What? Unsurprisingly, fintech is the sector attracting the largest amount of funding (57%, $1.6bn+, half of which was raised in Nigeria), followed - much much behind - by energy (~$300m) and education/jobs (~$250m, driven by Andela’s recent $200m Series E).

By Whom? 94% of the funding has been raised by start-ups with a male CEO. Male single founders and all-male founding teams represent 78% of the funding raised (down from 84% a few days earlier, thanks to the Andela deal - For more, see our recent post on the topic). Their female single founder and all-female founding team counterparts however only attracted 0.6% of the total funding raised.

From Whom? Almost 600 investors have already been involved in at least one $100k+ deal in Africa this year so far. The majority of them (72%) have participated in only one deal; some however have been extremely active (For more, see our recent post on the Top5 investors of 2021)

Thanks for reading us this week :) And as usual, don’t hesitate to get in touch if you have any questions, or want to know more about the database of deals we’re using to crunch all these numbers.