May 2026: More "Meh" than "Yay"

Despite an improvement in deal flow, the total amount raised remains underwhelming

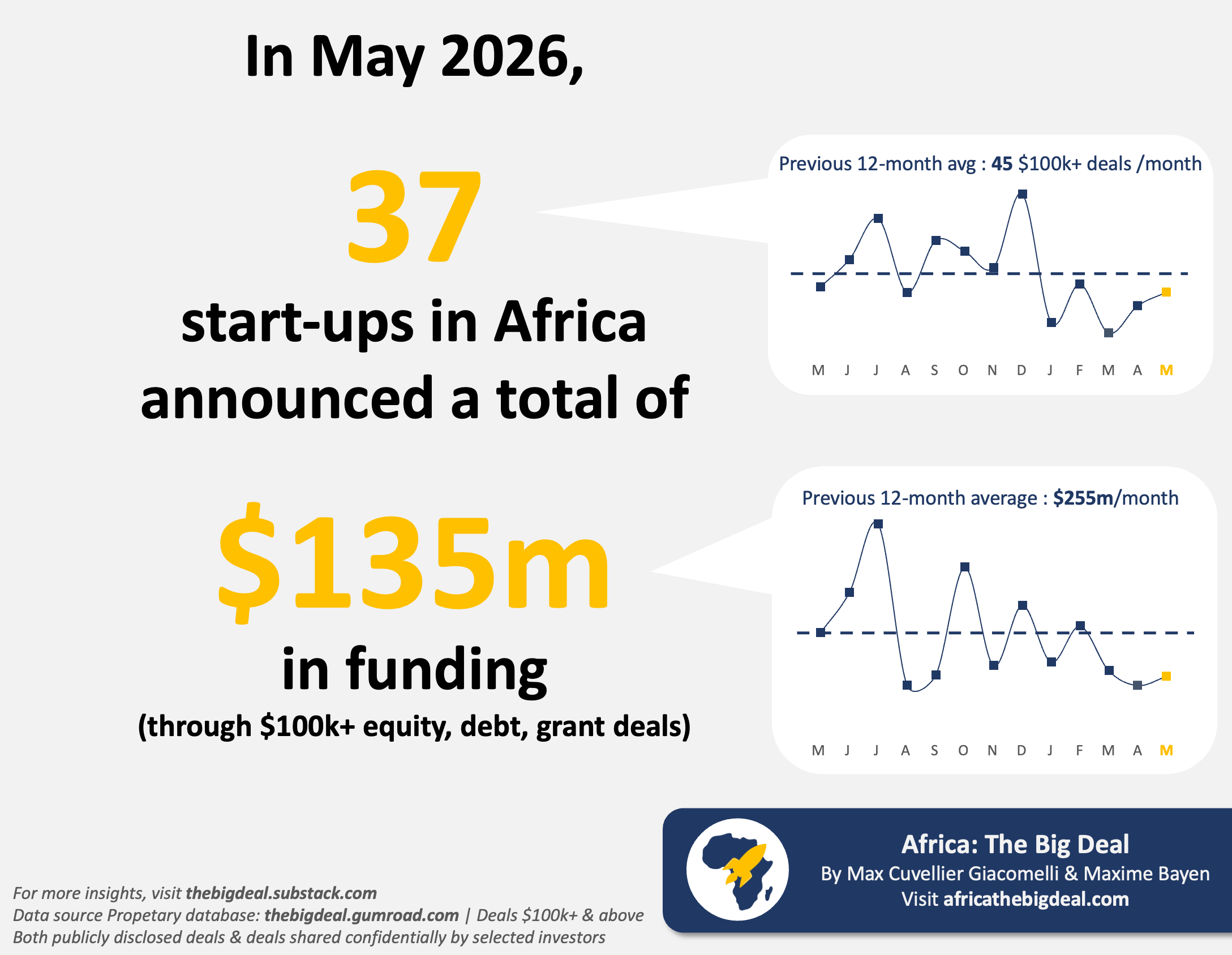

37 start-ups in Africa announced a total of $135m in funding through $100k+ deals (equity, debt, grants; excl. exits) in May 2026. Deal activity improved again after April (32) and the March low (22), but remains below the previous 12-month average (45 deals/month). From a total funding raised perspective, May was better than April ($110m) but lower than March ($150m), and significantly below the previous 12-month average ($255m/month).

The more structural signal sits again in the instrument mix. May was almost perfectly balanced between equity ($65m) and debt ($68) (with an extra $2m in grants). And that balance is not just a May quirk: it’s broadly what the market looks like now, a marked shift from 12–18 months ago, when the ecosystem was much more equity-led, with an equity share over 70%. In terms of how many ventures raised by instrument, equity continues to lead: 22 ventures raised equity, 7 raised debt, and 8 raised (small) grants. Zooming out, the year-to-date picture reinforces that same story. 2026 YTD (Jan–May) now stands at $843m across 160 $100k+ deals, split almost evenly between equity and debt. In other words: deal flow is recovering off March’s trough, but the market’s “engine” remains the same, with debt doing a lot of the work to keep totals afloat.

May’s headline total was also heavily shaped by four transactions: Nala’s $50m credit facility, LemFi’s $30m Series B extension, Africa GreenCo’s $10m raise, and Bfree’s $10m round add up to $100m, i.e. roughly three quarters of the $135m announced in May. We also recorded six exits in May (not counted in the totals). One deserves a specific mention: Ghana-born insure tech pioneer Bima - whose corporate footprint has long since expanded globally - is being acquired for $119m. That’s a meaningful reminder that, even in a month where primary funding totals remain muted, liquidity events are still happening in the background, and sometimes at non-trivial sizes.

While the sample is small, we can note that geographically, West Africa and East Africa attracted ~85% of the total amount raised in May (Nigeria alone accounted for ~64% of all equity raised across the continent), though the picture is more balanced when you look at deal count, not just amount. Sector-wise, fintech once again did the heavy lifting on amount raised driven by both the Nala and LemFi tickets. The signal is familiar: a reasonably diverse set of ventures getting funded, but a disproportionate share of the amount raised still hinging on a handful of larger transactions.

Net-net, May looks consistent with the emerging 2026 “new normal”: 30–40 deals/month, $100m–$200m/month, and a funding mix where debt plays an outsized stabilising role. That profile is notably softer than 2025, when the market’s run-rate was closer to ~50 deals/month and ~$300m/month across the year, and the mix materially more equity-led. But the June 1st Spiro announcement - and hopefully more of the like - might help prop up the H1 numbers. We’ll know that in month’s time…

If you want to go beyond the headline chart and numbers, our database lets you pull the full May deal list (and the underlying sources), slice it by country/region, sector, stage and instrument, and benchmark against any month or rolling window since 2019. It also includes an ever-growing set of deals shared confidentially by selected investors, so you’re not just reading what made the news. If you don’t have access yet, grab it here with a discount. Ciao! Max

At least it's no longer looking like the early stages of a bubble.