March 2026: Amount is fine. Deal count isn't.

A decent $150m+ month on paper, but the lowest monthly count of ventures raising $100k+ we’ve seen since 2021...

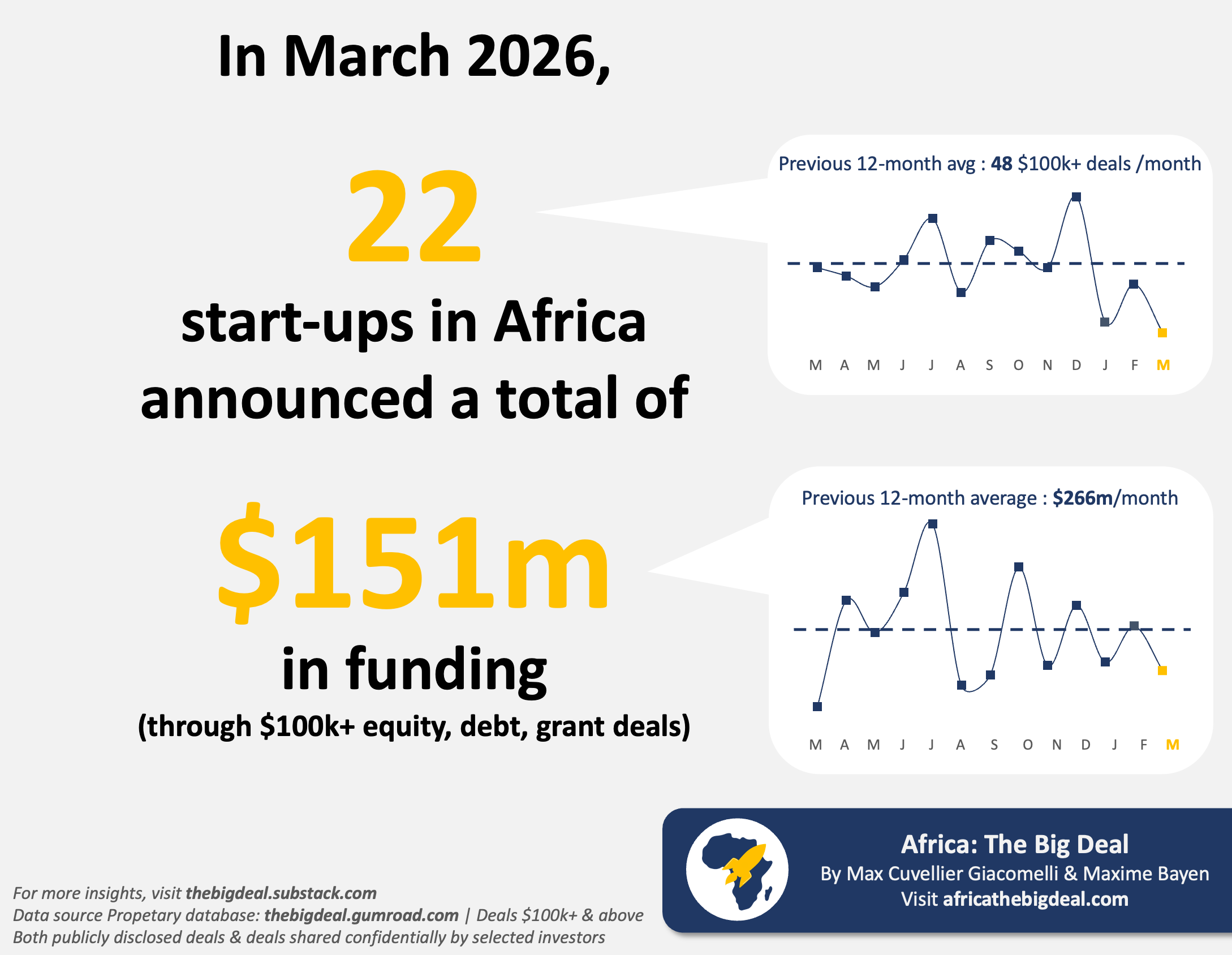

In March 2026, 22 start-ups in Africa announced a total of $151m in funding through $100k+ deals (equity, debt, grants; exc. exits). From an amount perspective, while this is nearly three times what was raised a year ago in March 2025, it’s still well below the monthly average of $266m we’ve observed over the past 12 months (that average is itself made up of serious highs ($554m in July 2025) and lows ($52m in March 2025)). That said, we know month-to-month moves are an unfairly volatile metric. And if we focus on the 12-month rolling picture, it still fits neatly with the pattern we studied in a recent post: in the 12 months to March 2026 (Apr 2025–Mar 2026), start-ups in Africa raised $3.3b (exc. exits), including $1.8b in equity and $1.4b in debt. If anything, these numbers sit towards the top end of the band.

Early-stage African founders: applications for the 2026 FINCA Ventures Prize are still open until April 16. Compete to win up to $100k in catalytic grant funding to scale bold, tech-driven fintech solutions for financial inclusion or sustainable agriculture. Agri & Food ventures may also apply for technical assistance through the CLIC Connector program. If you’re building for impact, this is a great opportunity. Don’t miss it!

March was overwhelmingly a debt month: of the $151m raised, $55m was equity and $96m was debt, meaning nearly two thirds of the month’s total came as debt. As usual, a handful of deals concentrated quite a bit of the funding. Sistema.bio led the month with $53m in debt, MNT-Halan followed with another bond issuance worth $40m+ this time, and Zeno rounded out the top three with a $25m Series A. Exits were also busy in the background: we recorded five of them in March (all values undisclosed), with the most talked-about being Orda’s acquisition by Moniepoint.

With March in the books, Q1 2026 (Jan–Mar) comes in a couple millions short of the $600m mark, split almost evenly between equity ($291m) and debt ($304m), across 83 ventures. That’s a very different shape from Q1 2025, when start-ups had raised less ($469m), but the mix was far more equity-led ($397m vs $52m debt, i.e. 89% equity), and 130 ventures had contributed to the total.

There are clearly fewer start-ups raising this year so far, and this is part of an almost uninterrupted downward trend since the heatwave. We’ll come back to this in a future post, but the venture count is the immediate cause for concern: 22 start-ups raised in March, and this is the lowest monthly count we’ve seen since we started tracking $100k+ deals in 2021. In particular, only 130 ventures raised between $100k and $500k in equity in the past 12 months, and this is again the lowest that rolling count has been since at least 2021. Despite the funding winter, a year ago that number was 150+. So while the total amount raised is holding up at a decent level, it increasingly relies on a few larger (debt) tickets, once again raising questions about future prospects if early-stage ventures remain underfunded…

If you want to go beyond the headline chart and numbers, our database lets you pull the full March deal list (and the underlying sources), slice it by country/region, sector, stage and instrument, and benchmark against any month or rolling window since 2019. It also includes an ever growing set of deals shared confidentially by selected investors (so you’re not just reading what made the press). If you don’t have access yet, grab it here with a discount. Ciao! Max