April 2026: Total amount hits a 13-month low

Deal activity rebounded slightly from March, but the total amount raised fell to its lowest level in over a year

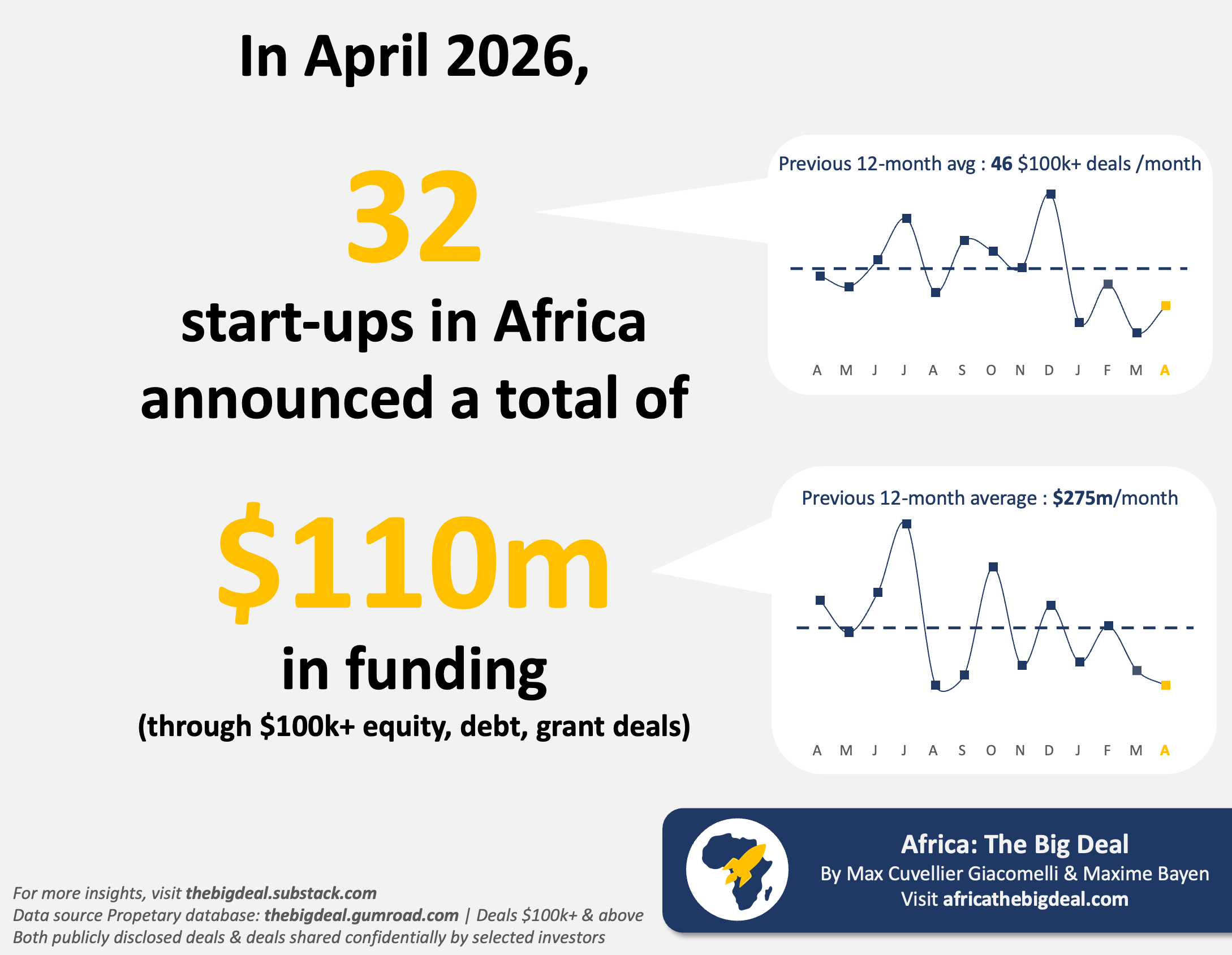

In April 2026, 32 start-ups in Africa announced a total of $110m in funding through $100k+ deals (equity, debt, grants; exc. exits). From a deal activity point of view, that’s a welcome bounce from a very slow March (22), yet still very much below the previous 12-month average of 46 deals/month. As far as total amount is concerned, April’s $110m is the lowest monthly tally since March 2025 ($52m), and well below the previous 12-month average of $275m/month.

That said, we know month-to-month moves are unfairly volatile metrics. And if we focus on the 12-month rolling picture, the total raised still fits neatly within the band we’ve been tracking for a few months now: $3.1b (±$90m) since August 2025. Indeed, in the 12 months to April 2026 (May 2025–Apr 2026), start-ups in Africa raised $3.1b (exc. exits), including $1.7b in equity and $1.4b in debt (plus $30m in grants). The rolling total amount is still holding up, propped up by debt performance.

If April’s total amount was lower than March’s overall, it was higher on equity: $74m came as equity and $36m as debt, while March had been overwhelmingly debt-led ($55m equity, $96m debt). As usual, a handful of deals concentrated a large share of the month’s total: Egyptian fintech Lucky raised a $23m Series B, while Gozem ($15.2m debt) and Victory Farms ($15m debt) did most of the heavy lifting on the debt side. Ethiopia-based electric mobility start-ups Dodai announced $13m ($8m Series A + $5m debt). April also saw two exits: Nigeria’s Bread Africa was acquired by SMC DAO as consolidation continues in the country’s digital asset sector, and Egypt’s waste recycling start-up Cyclex was acquired by Saudi-Egyptian investment firm Edafa Venture.

With April in the books, 2026 YTD (Jan–Apr) comes in at $708m across 124 $100k+ deals (exc. exits), split almost evenly between equity ($364m) and debt ($340m). That’s a pretty different profile from Jan–Apr 2025 for instance, when start-ups had raised more ($813m, -13% YoY) across far more deals (180, -31% YoY), and with much more equity-led mix ($652m equity vs $138m debt, 80%/20%). So far this year we’re seeing the same underlying pattern: fewer ventures raising, and a greater reliance on debt to keep totals afloat…

If you want to go beyond the headline chart and numbers, our database lets you pull the full April deal list (and the underlying sources), slice it by country/region, sector, stage and instrument, and benchmark against any month or rolling window since 2019. It also includes an ever growing set of deals shared confidentially by selected investors (so you’re not just reading what made the press). If you don’t have access yet, grab it here with a discount. Bom dia! Max