As flat as the top of Table Mountain 🚠

12-month rolling funding has now been stable for 7 months. Below the heatwave peak, above the winter lows, and structurally more debt-driven.

🚀 Unveiling our 'Data for Founders' initiative

If you haven’t yet applied to our ‘DATA FOR FOUNDERS’ initiative - in partnership with FMO Ventures - to get 2 years of 🆓 access to our start-up deals database (and more), make sure to do so by the deadline. We have just extended it until 🚨 March 27 🚨... though that’s not an excuse to delay your application until the last minute!

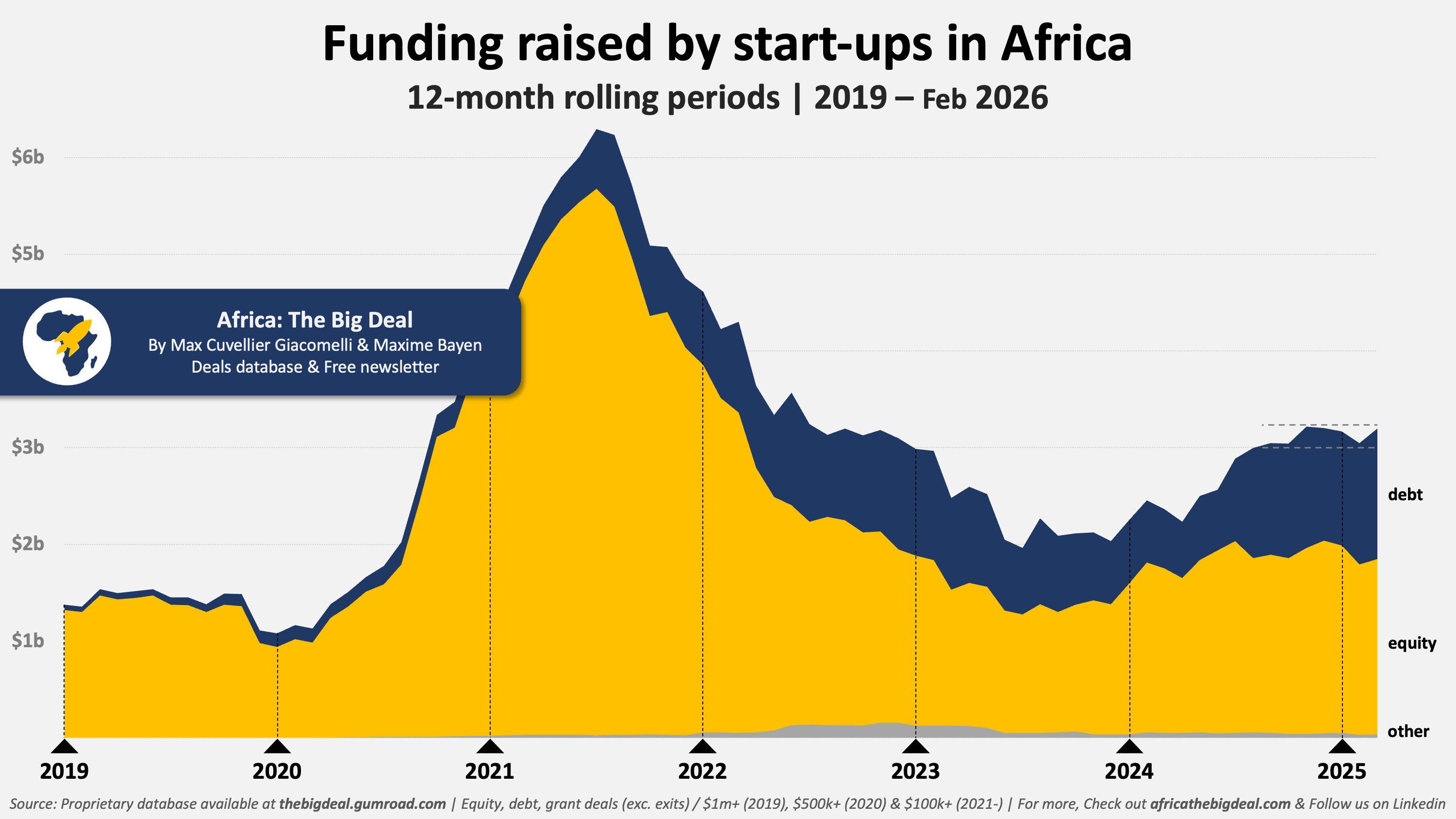

While it is helpful to follow the evolution of start-up funding on a monthly basis, for most of us who are in it for the long haul, long-term trends are much more telling. This is why this week I wanted to update an analysis I have done in the past, that focuses on 12-month rolling periods, and therefore smoothes out monthly variations and seasonal effects. And something comes out very clearly: start-up funding in Africa has reached a new cruising speed since mid-2025, and it’s held to it very steadily since.

Most of you will already be familiar with the different ‘chapters’ we have seen play out, with funding accelerating at breakneck speed from mid-2021 onwards, peaking in mid-2022 at a staggering ~$6.3b (July 2021-June 2022), then falling through 2023 and reaching a low point of ~$2b two years later (July 2023-June 2024) - still higher that pre-heatwave levels though -, and then back on a more modest growth trajectory.

That’s where the recent plateau comes in: since August 2025, 12-month rolling funding has sat in a pretty tight band around $3.1b (±$90m). That kind of stability is rare since 2020, except for another plateau in late 2022 post-heatwave, before the numbers started to slide further. Over the past few months, not only has funding been stable, but so is the case for the rolling number of ventures clearing meaningful thresholds: the count of ventures raising $1m+ or $10m+ for instance are holding steady around 211 (±5) and 65 (±4). These numbers have actually been relatively flat since as far back as mid-2024, as opposed to dollar amounts. In plain terms, the ecosystem seems to have found a stable run-rate, at least for now.

Another interesting point is what this new normal is made of. Pre-heatwave, the market was overwhelmingly an equity story. Today, debt has become an important pillar of start-up financing on the continent. In the current plateau, debt represents roughly two-fifths of funding (39% ±3%). Since August 2025, 12-month rolling equity funding has been around $1.8b (±$125m) and debt around $1.2b (±$125m). This is the clearest structural change in the data: stability is back, but with different mechanics, and more maturity.

One final comment on the early-stage engine, to insist on a point Grégoire de Padirac made in his guest post back in January. The $100k–$1m layer is certainly thinner in deal volume than it was during the heatwave. But relatively speaking, this is not a “small-deals-only” phenomenon: the contraction in the number of ventures raising $100k–$1m since the heatwave is broadly comparable to the contraction in ventures raising $1m+, at least in relative terms. So the story of the past couple of years is not that the base fell out while the top stayed intact. But if this is truly the new cruising speed, the challenge is clear: can the market keep funding enough new entrants to build a pipe of future larger deals, without needing another heatwave to boost immediate and future growth?

If you need access to the underlying data ready to be sliced by country, sector, stage, or investor, that’s what our Africa: The Big Deal database is for. You can access it here at a discount. Or if you’re a start-up and feeling lucky, apply to join our ‘Data for Founders’ initiative - in partnership with FMO Ventures - for a chance to get free access to the database for the next two years (and more). Have a good day! Max