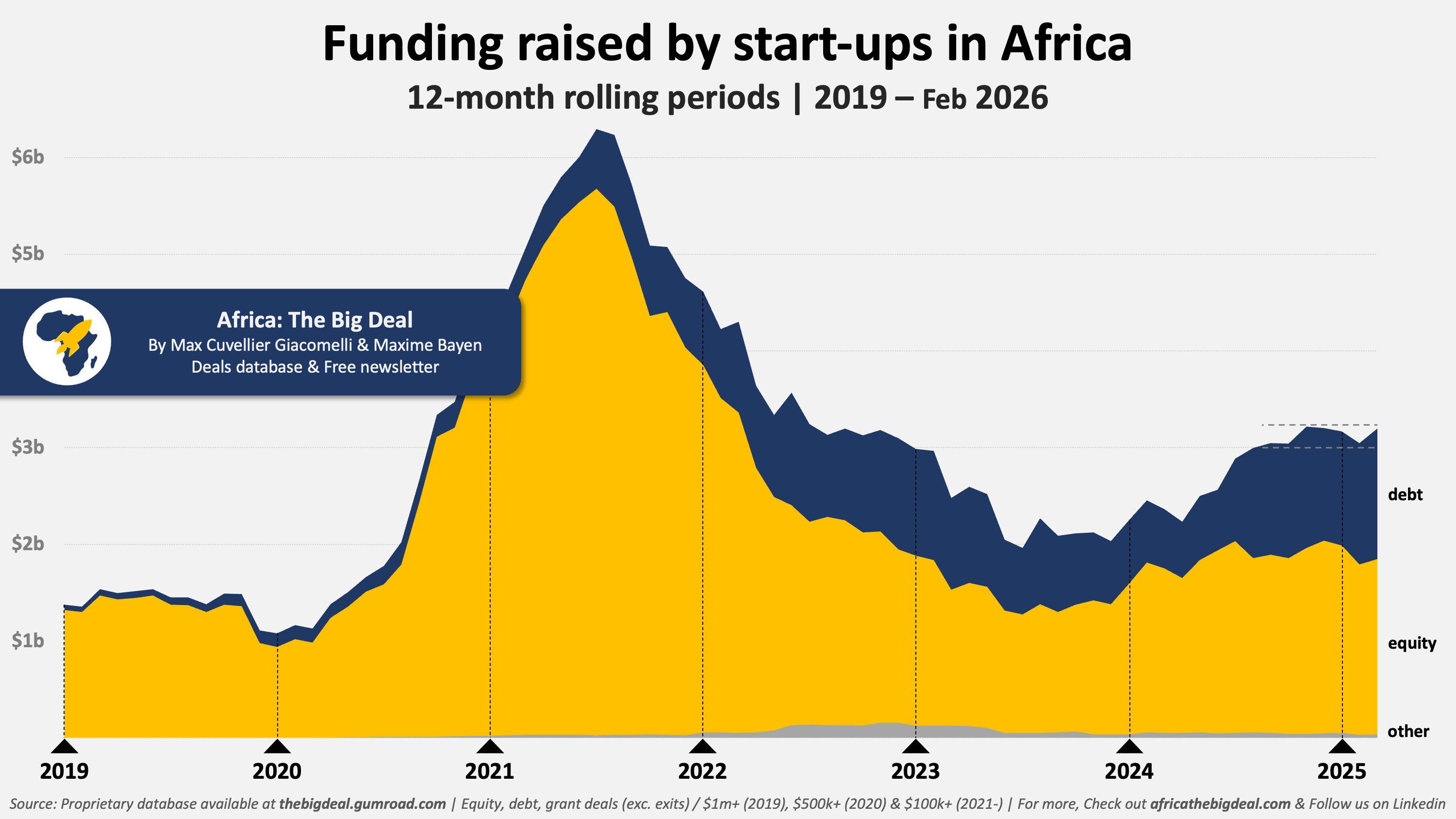

Since the heatwave in particular, debt has emerged as a core feature of the start-up funding landscape in Africa. Debt has its own merits and it would be wrong to somehow oppose it to equity. This is not a competition, but a partnership. Debt and equity investors - and those do both - play very different yet equally important roles in a maturing start-up ecosystem. This week, we dig deeper into our database to see what key trends we could identify on the debt front…

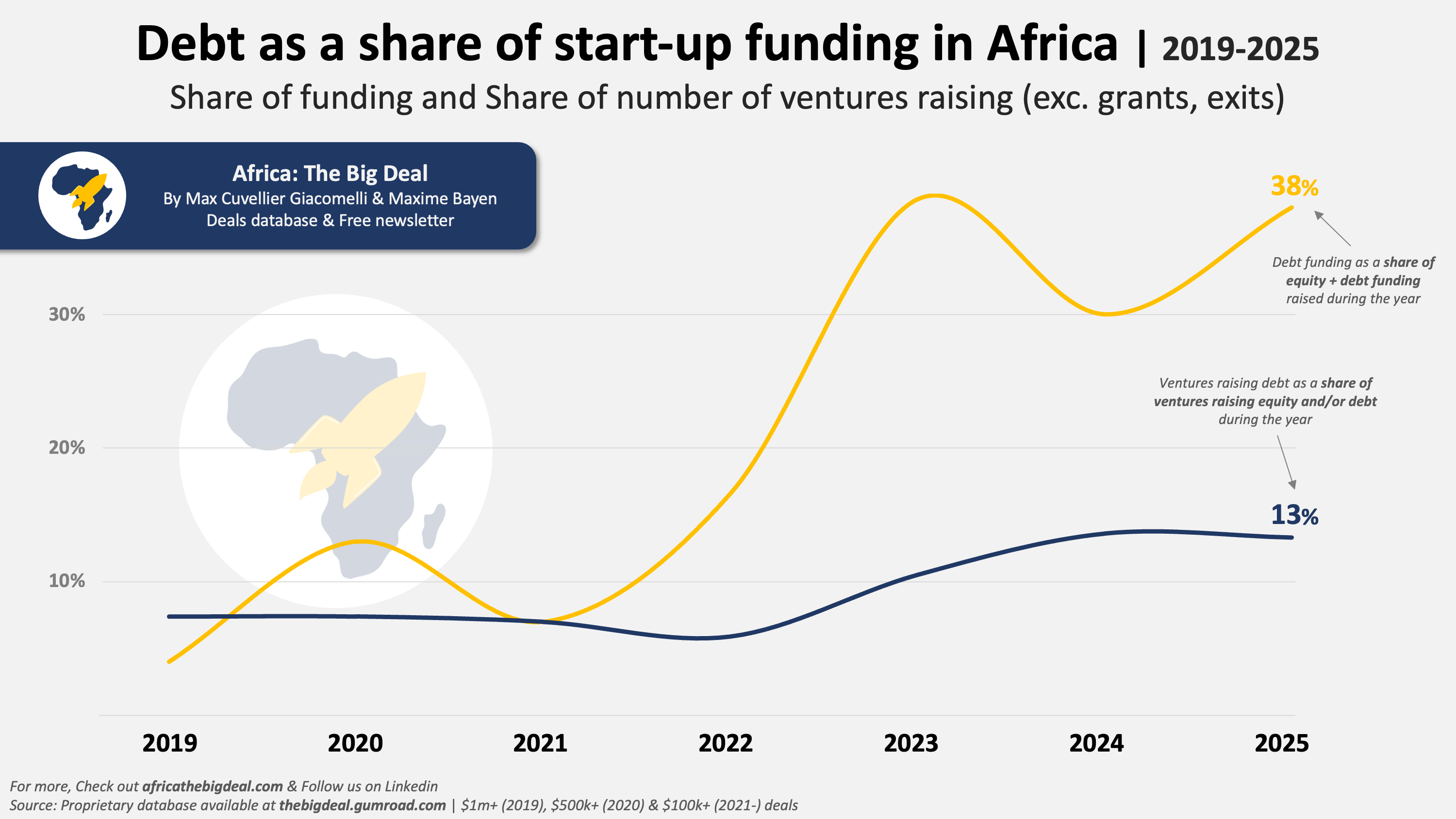

1️⃣. Debt is now a material part of the funding story. Announced debt grew from less than $300m in 2021 to $1.2b in 2025. Over the same period, debt’s share of total disclosed start-up funding (exc. grants & exits) rose from 7% to 38%, making it a meaningful part of the market rather than a niche side-note.

2️⃣. But debt still reaches relatively few ventures. Between 2021 and 2025, 169 start-ups announced a debt round, versus 1,880 that announced equity funding: roughly a 1 to 11 ratio over the period. That gap has narrowed, though: in 2025, the ratio was closer to 1 to 7, with 53 start-ups announcing debt against 363 announcing equity (13%).

3️⃣. Most debt is announced on its own, not alongside equity. In 2025, 87% of debt-raising start-ups announced just debt, as opposed to debt tied up to an equity round. That is up from 75% in 2022-2023, suggesting debt is increasingly being used as a standalone financing tool rather than an add-on to an equity raise.

4️⃣. The typical debt round tends to get bigger. The median disclosed debt round was $2m in 2021, $5.5m in 2022, $3.6m in 2023, $2.1m in 2024, and $5m in 2025. So while the market has clearly matured, it has not done so smoothly: progress has come in jumps, setbacks, and rebounds.

5️⃣. A handful of mega-deals still define each year. In every year from 2021 to 2025, the single largest debt round represented between 18% and 26% of all disclosed debt raised that year. For instance in 2025, d.light’s $300m facility alone accounted for roughly a quarter of all announced debt, which helps explain why annual totals and medians can swing quite sharply.

6️⃣. Debt is much more concentrated than equity. Since 2019, the top 10 debt raisers (d.light, MNT-Halan, Sun King, M-Kopa, Wave, Moove, Spiro, valU, Planet42 & Burn) have accounted for roughly 66% of all disclosed debt raised, versus just under 25% for the top 10 equity raisers (Opay, MNT-Halan, TymeBank, Flutterwave, Sun King, Interswitch, M-Kopa, Chipper Cash, Andela & Moove), with four companies making both top 10 lists (MNT-Halan, Sun King, M-Kopa & Moove). In most years, the top 10 debt raisers capture 75-80% of the annual total, while for equity the equivalent range is closer to 40-50%.

7️⃣. Energy and Fintech dominate debt. Add Transport & Logistics, and you have almost the whole market. Between 2021 and 2025, Energy + Fintech represented about 60% of debt deals and roughly 83% of total announced debt. With Transport & Logistics, that rises to roughly 76% of debt deals and more than 93% of the total, showing just how concentrated debt remains in a small set of sectors and business models.

8️⃣. West Africa often leads by number of debt deals; East Africa often leads by amount of debt raised. West Africa regularly contributes the largest share of debt deals, while East Africa repeatedly captures the largest facilities, especially in the Energy sector. But this is exactly where concentration matters: one or two very large rounds can redraw the regional picture in a single year.

9️⃣. African start-up debt is not one market. It is at least four. The lender base breaks down into crowd/retail platforms (e.g. Lendahand, Bettervest, Trine), DFIs and public institutions (e.g. IFC, BII, DFC), commercial banks (e.g. Standard Bank, CIB, Rand Merchant Bank), and specialist non-bank lenders such as private credit or structured debt funds (e.g. Symbiotics, Lendable, Verdant). Those are not just different capital providers; they are different products, different underwriting logics, and often different sector or geographical preferences (especially for commercial banks).

🔟. The lender mix is becoming much more institutional. In 2021, crowd and retail lenders still appeared in about 35% of debt deals; by 2025, that figure was down to about 3%. Over the same period, DFIs, banks, and especially specialist non-bank lenders became much more visible, suggesting the market is moving away from smaller platform-led debt and toward more structured institutional financing.

Again, the point is not that debt is overtaking equity. It is that debt is becoming a more important layer of the African start-up funding stack, with its own logic, its own repeat players, and its own patterns. To some extent, it remains a selective instrument, available to a relatively small number of later-stage ventures and heavily skewed toward a few sectors and large borrowers. But it is no longer an exception. It is becoming part of the market’s core plumbing.