Where are the investors? 🔭

In line with the drop in number of deals being signed, the number of investors signing checks in 2026 so far is declining

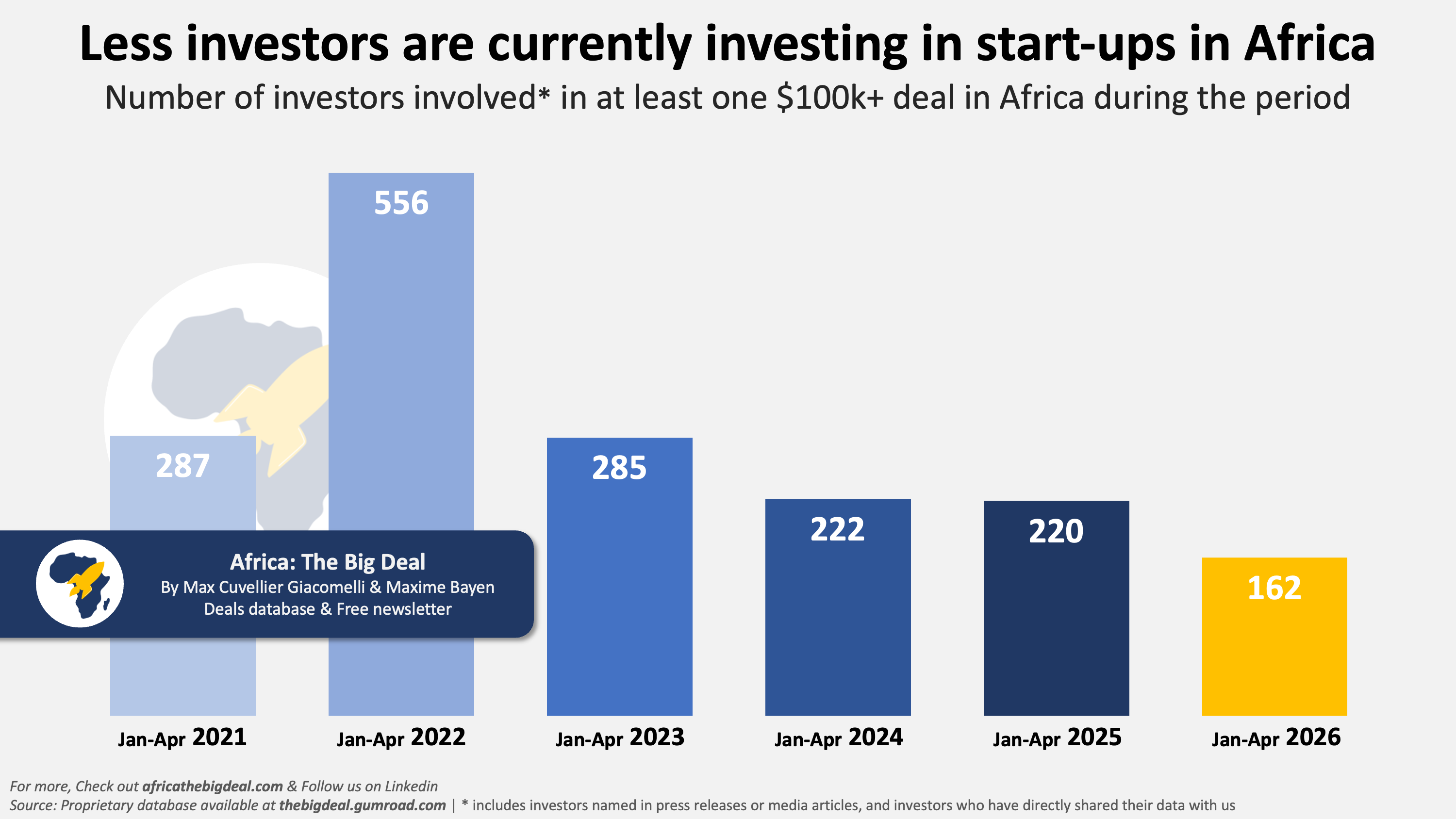

In the first four months of 2026, we recorded 162 unique investors participating in at least one non-exit $100k+ deal on the continent. This is the lowest Jan–Apr count we’ve seen since we started tracking comparable data in 2021. (While we can’t capture every single investor’s involvement, particularly where checks are smaller or disclosure limited, our methodology has been unchanged since 2021, allowing for comparability). Since the 2022 spike (556), participation stabilised in 2024 (222) and 2025 (220), but now seems to be contracting significantly in 2026 (-26% YoY). This drop in investor participation is tightly linked to the shape of the market with Jan–Apr 2026 recording only 124 deals (exc. exits), significantly down versus recent Jan–Apr windows.

Even in this context, some investors have continued to ‘show up’ in the first four months of 2026. A few names have appeared repeatedly, helping keep momentum, including DEG who announced 11 new grants via their developpp programme (in EVMAK, Rada 360, Sumet Technologies etc.) and Azur Innovation Fund who was involved in four new equity investments in Morocco (Enakl, Weego, Goswap & ZSystems). Beyond these, we find a layer of familiar names, active participants in the ecosystem who continue to anchor early-stage and growth syndicates, including IFC, Enza Capital, Norrsken 22, Global Innovation Fund, Digital Africa, Launch Africa, Partech and Madica who were active in at least three $100k+ deals each, and an extra 20 investors who participated in two $100k+ deals, and potentially more*. While the overall set of active participants is smaller in 2026 so far, the market still benefits from a core of repeat actors that can provide continuity.

Geographically, the investor base is broadly stable, with two notable shifts. Among investors with known HQ active on the continent in Jan–Apr 2026, Africa leads with 36% (56), followed by the US (25%), Europe (19%), APAC (13%), and the Middle East (6%). This is largely aligned with the post-2022 pattern, except Europe’s representation is lower (19% vs ~26% average across Jan–Apr 2023–2025) and APAC’s higher (13% vs ~6%). APAC’s uplift is primarily a Japan story: 12 of the 20 APAC investors active in Jan–Apr 2026 were Japan-based, boosted by Japanese participation in the Dodai and Sora Technology deals (each with five Japanese investors listed). Within Europe, it seems that so far the UK and Germany might be holding up better than France and the Netherlands in terms of the origin of investors involved in at least one deal, but it is frankly too early to call as the samples are very small.

As always, this week’s data is coming from our proprietary Africa: The Big Deal database through which we have been tracking start-up investment activity on the continent since 2019. The full dataset can be accessed for a modest $18 a month if you use this discount link. Your support in sharing our work with your network - either the database or this free newsletter - continue to be much appreciated. Bonne journée! Max

*There can be a delay in how deals are reported, as we capture data from both public sources, and confidential disclosure from investors. If you’re an investor on the continent and think we might be missing some of the deals you have been involved in, please reach out to us.

The drop in unique investors is less about conviction and more about the cost of diligence in markets where information still travels slowly. The repeat players staying active are usually the ones with local networks that compress that cycle.