H1 2026: June saves the day! 😃

Thanks to an exceptional month of June driven by Spiro's $270m raise, H1's top line number ends up almost flat YoY

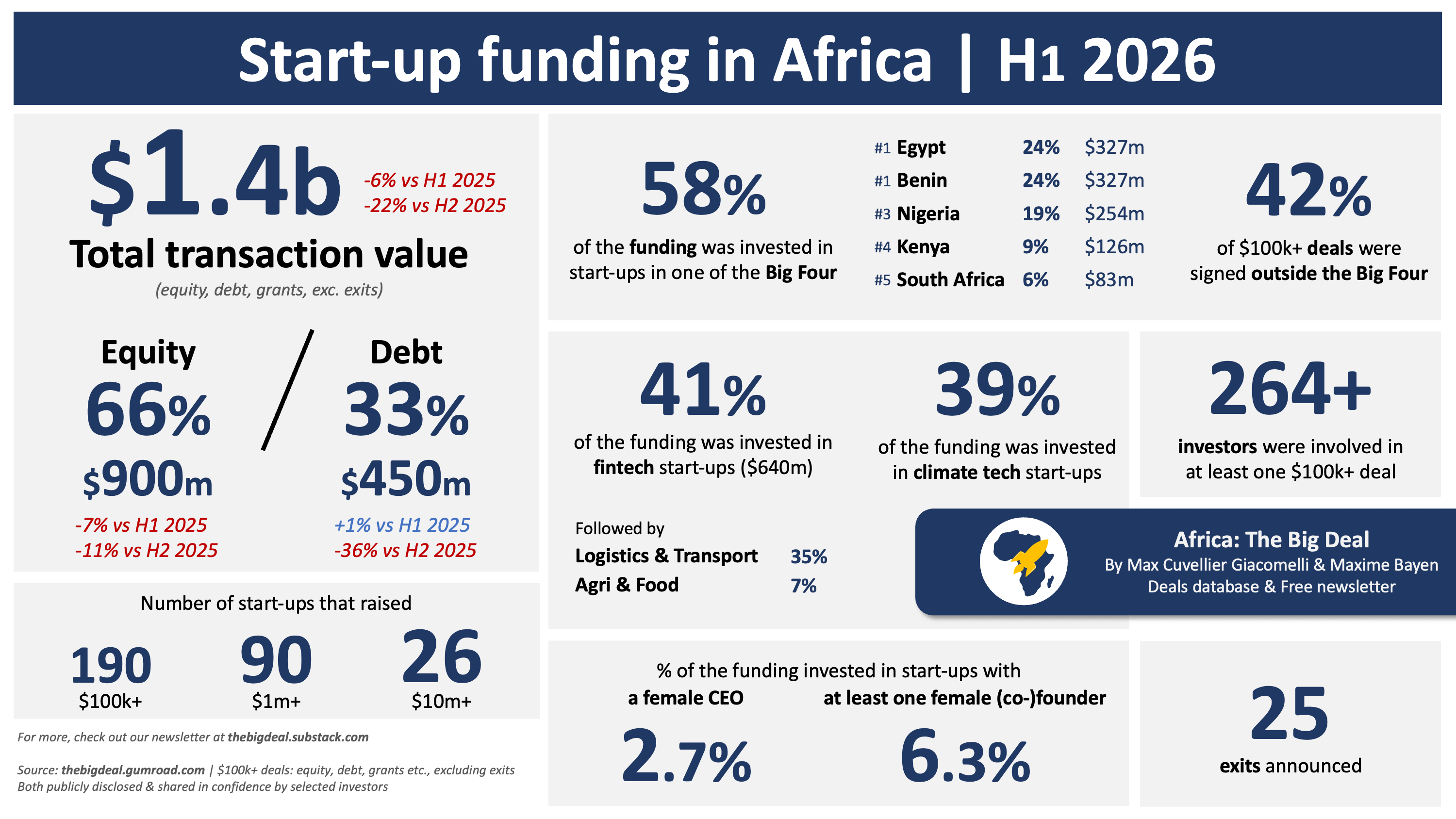

H1 is over. Long live H1 2026! Start-ups in Africa have raised close to $1.4 billion in funding in the first half of the year, pretty much on par with H1 2025. The total was split 2/3-1/3 between equity and debt. 190 ventures raised $100k+ during the period, and 264+ investors were involved in at least one deal…

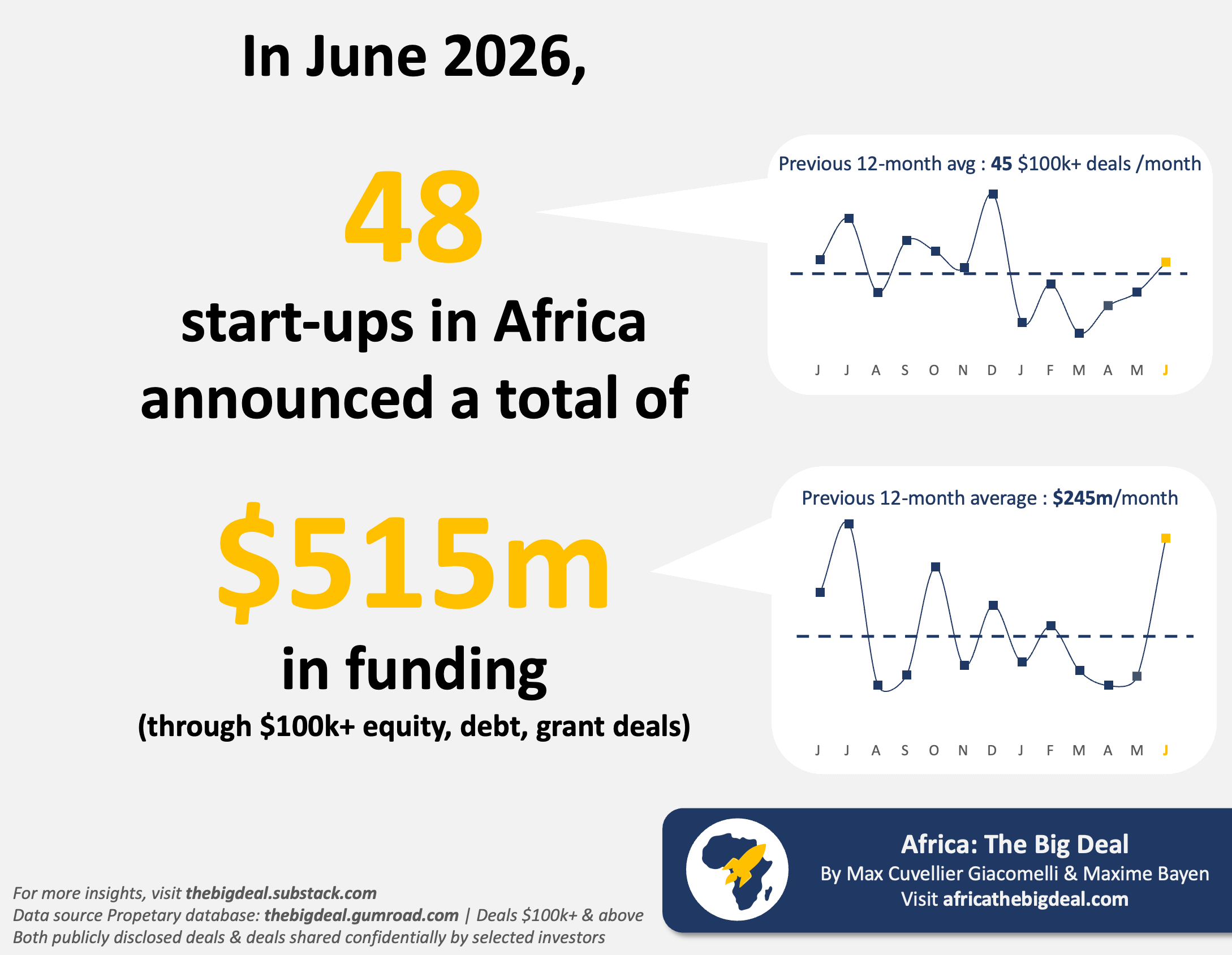

In the coming days and weeks, we will be diving deeper into these numbers, with our customary graphs and analyses. But first of all, we thought it was worth commenting on the June 2026 performance, which has certainly shaped H1’s overall trend. Indeed, at the end of May 2026, the numbers weren’t too encouraging. With ‘only’ $843m in the bag, the year to date total was tracking well below 2025: -21% YoY; and even -48% YoY for equity. Only February ($273m) had seen funding barely above the 2025 monthly average ($264m). And then June happened…

48 ventures raised $515m in June, way above what we had seen for a while. In fact, this was the best monthly tally since July 2025, and the second-best since early 2023. Most notably, 91% of the funding was raised as equity, after the equity-debt split had been roughly 50-50 until May. The $468m raised in equity were more than had been raised in the previous 5 months; it was nearly 3x times the average of the previous 12 months ($169m); and simply the best equity month since as far back as March 2022. There was undoubtedly a Spiro effect, as the venture announced a staggering $270m in funding in June, taking its total raised this year so far to $327m. No start-up had raised this much in a half-year since MNT-Halan in H1 2023 ($400m). Flutterwave also secured an estimated $100m Series E (a flat round, but as they say, ‘Flat is the new Up’) and MNT-Halan $50m. As a result, and despite a worrying start of the year, H1 2026 finished almost on par with H1 2025 for both total (-6% YoY) and equity funding (-7% YoY).

If this post has left you wanting more, you can explore the full dataset - over $21b worth of tracked funding and exit activity - by subscribing to our database. As always, we’ve arranged a discount for newsletter subscribers. And don’t worry, we’re far from done. Over the coming days and weeks, we’ll be digging deeper into the numbers: equity versus debt, sector trends, geographic split, gender lens, how Africa compares with the rest of the world, and plenty more. Thanks for reading, and see you again soon. Max

Nothing against Benin, but I think calling Spiro a Beninese company really is a massive stretch these days, as they have by far their largest staff footprint + market in Kenya. They refer to Kenya as their operational HQ and the UAE as their corporate HQ – Benin doesn’t get a special mention these days.

I think it’s important to give credit where credit is due, and while Spiro is clearly pan-African, a lot of their recent success is Kenya-fuelled, and in turn becomes an important proof point that we can scale climate tech in Kenya. I think it’s about time we reclassify Spiro as Kenyan.

Thanks for this great data & analysis, as always!

Martin