🐘2024🐘 All hail the big guys!

Two new unicorns made the news while half of the start-up funding went to just ten ventures in 2024

Previously, on Africa: The Big Deal: East Africa/Kenya continued to top the charts in 2024 while only West Africa/Nigeria managed to hold up… Full episode:

At the end of the day, what most people will remember about 2024 when it comes to start-up funding in Africa is probably the minting of two new unicorns. So let’s look at those for a minute, but also use this as a cue to interrogate how much of the funding in Africa is going to the ‘big guys’…

First, the so-called unicorns: in late October, Moniepoint announced its Series C and a valuation of ‘over $1b’ according to ‘sources close to the transaction’. A few weeks later in mid-December it was Tyme’s turn to announce a $250m round at a $1.5b valuation. This is impressive, but Why does it matter? Putting aside the (interesting) debate about whether new unicorns are a good proxy for ecosystem maturity, in the three years since the end of 2021 (when 5 start-ups gained unicorn status), only MNT-Halan had graduated to unicorn status, in early 2023. So these two back-to-back announcements somehow cocked a snoot at those arguing the start-up ecosystem on the continent was moribund... For more, check out:

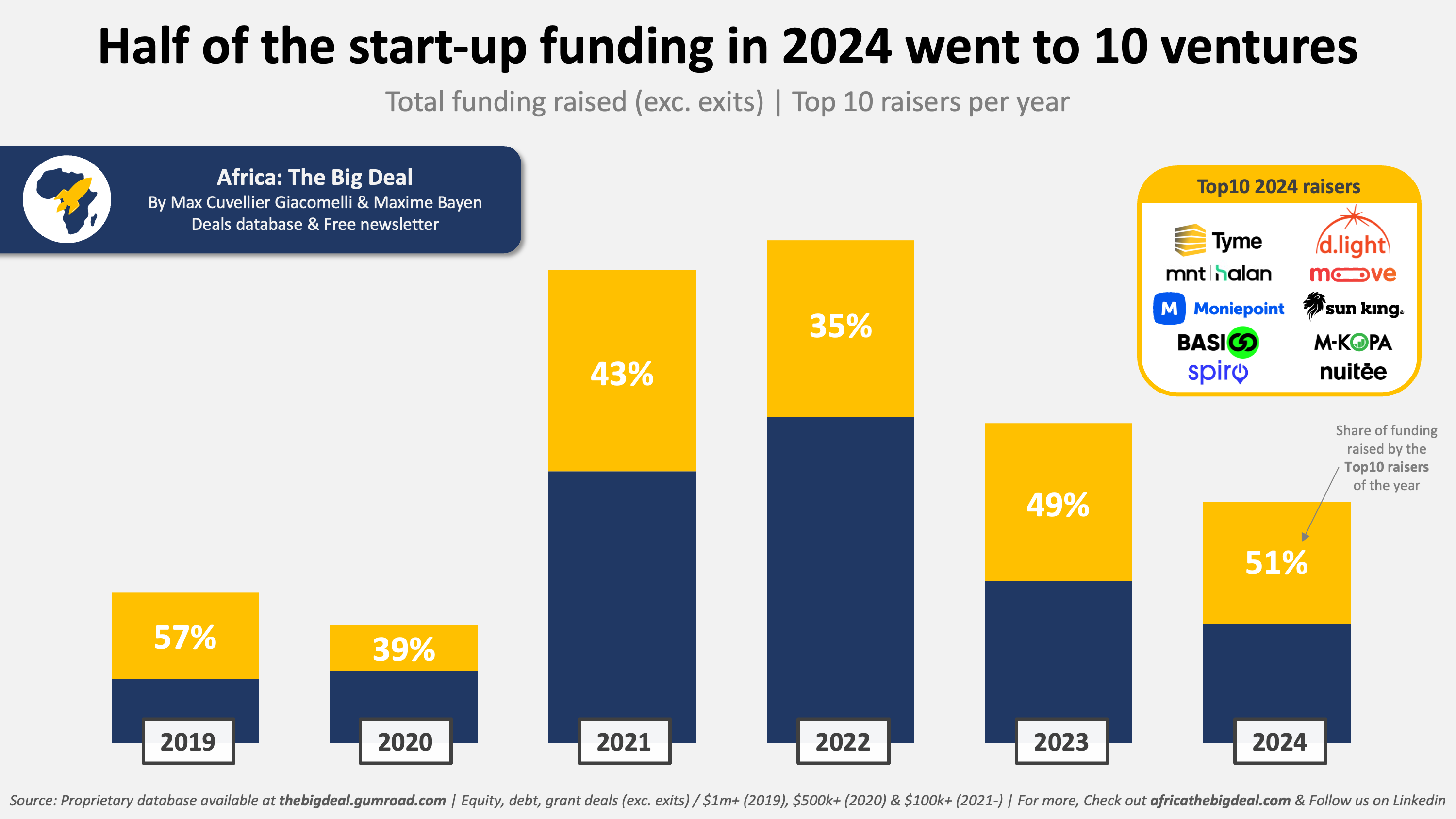

The Moniepoint and Tyme stories also offer an opportunity to look at how much large deals and ventures really weigh in the start-up funding dynamics. In short: A lot. In fact, Africa’s 9 unicorns have raised $3.9b in funding since 2019, almost a quarter (23%) of all the funding raised on the continent in the past 6 years. And it is not just about unicorns. If we look at the list of start-ups that have raised $100m or more since 2019 (including of course the 9 above-mentioned unicorns), we find 28 of them in total, out of 2,000+ ventures that have had some fundraising activity over $100k in the period. Collectively, they have raised $7.8b since 2019, i.e. almost half (47%) of the total invested. And the concentration of funding in the hands of the ‘big guys’ doesn’t seem to be going away…

🎙️ There is just over a week to go until our Linkedin Live on January 16. What will we be talking about? Everything start-up funding in Africa, basically. Don’t miss out, and make sure you mark your calendars by registering here :)

In fact, the Top10 raisers in 2024 attracted 51% of the funding. This is the highest proportion since 2019, and pretty much in line with 2023 dynamics. Who were they? Moniepoint and Tyme of course, but also two other fintechs (MNT-Halan & M-Kopa) and four ‘climate tech’ ventures (either solar: d.light, Sun King; or EV: Basigo and Spiro); plus moove and nuitée. Unsurprisingly, eight were located in a ‘Big Four’ country. Actually, of the 42 ventures that raised $10m or more in 2024, 86% were HQ’ed in a Big Four market.

Finally, if we look on the other end of the spectrum, at the ventures raising small tickets ($100k and over), we see that the ‘bottom 80%’ (i.e. the 345 ventures that raised the least) attracted just 11% of the funding in 2024. While this might seem small, this ‘long tail’ effect isn’t unexpected, and these ventures should not be overlooked, as the small deals of today will - hopefully - be the big deals of tomorrow…

We’re going to stop here for this week, because we’ve given you a lot to think about already, and because we don’t want you to start feeling like we’re spamming you 😜. But we’ll be back in earnest early next week. In the meanwhile, if you’re hungry for more data, our database should content you. And we suggest you access it here so you can benefit from a little discount…

👉UP NEXT👉 Does fintech still rule world? Get ready for our analysis of trends by sector as we put our green tinted glasses on…