Out of the woods? Looking at what could well be a 'new normal'...

A fresh look at the data brings a new perspective on the so-called 'funding winter'

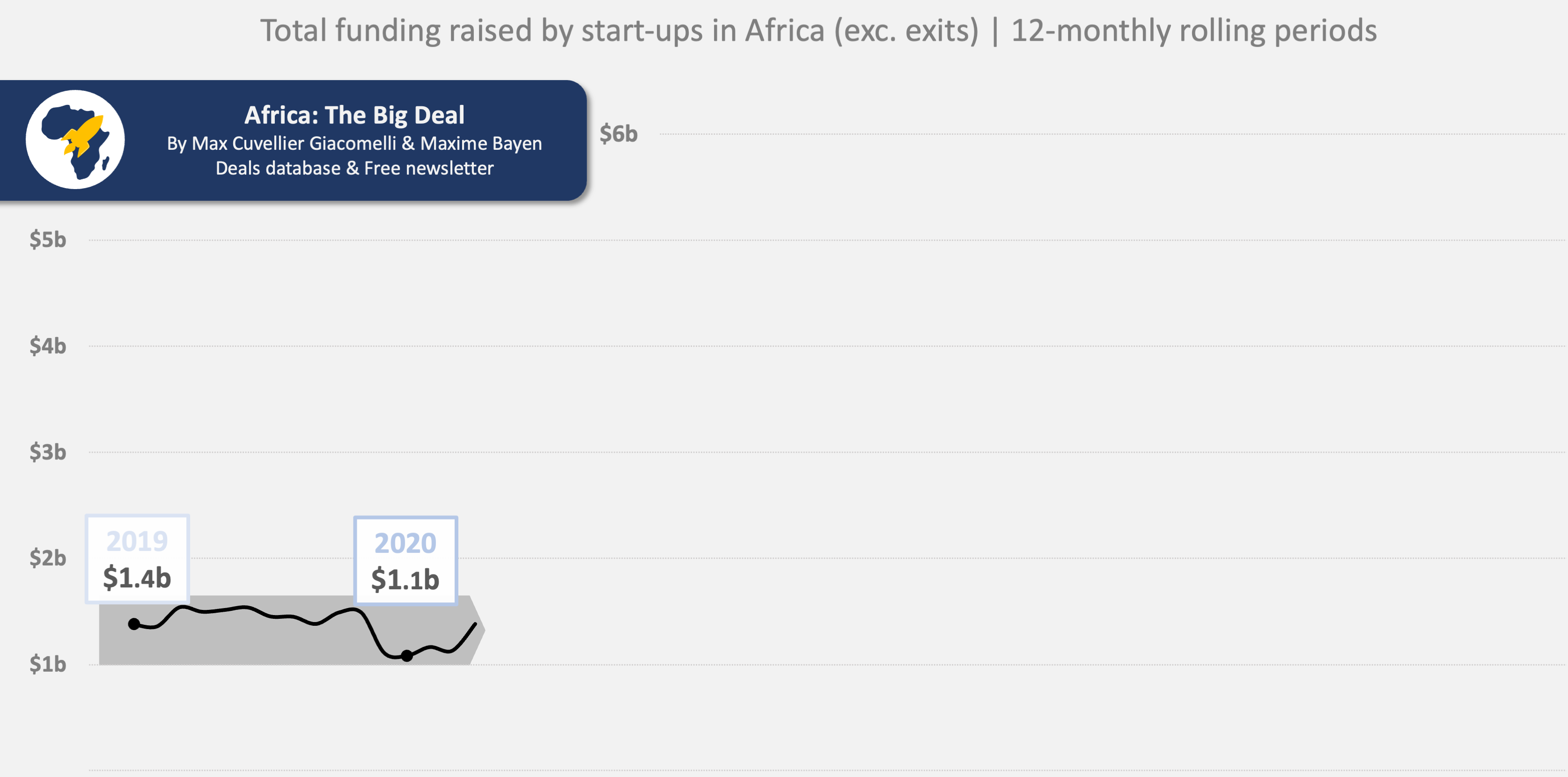

Data can sometimes be misleading if you don’t step back enough to look at it, especially if you’re trying to identify trends. For instance, while we do share monthly tallies, I don’t do monthly analysis. It’s just too volatile. (As a matter of fact, March wasn’t good in terms of start-up funding in Africa ($50m), yet a week into April, more funding has already been announced than in March and February combined). Quarterly aggregates are a little better. But still. Yearly data is good, yet it arbitrarily puts the cutting point on December 31st, which can make us miss the point.

I personally like 12-monthly rolling periods. They’re better at picking up shifts in gears (whether it’s an acceleration or a deceleration), but also periods of stability. Could this be the key to better understanding the recent dynamics in the ecosystem? Could it challenge the pessimist view that 2024 was another year of decline? Well, Well…

Since we started collecting the data in 2019, and until things got hot in mid-2021, funding on the continent was actually pretty stable: there is little variance over the 2.5-year period, with a minimum of $1.1b raised over any 12-month period, a maximum of $1.5b, and an average of $1.4 billion.

Then things went (a bit) crazy. Like in the rest of the world - though it started a few months later on the continent -, start-up investments exploded, reaching a peak of $6.3 billion raised between mid-2021 and mid-2022, i.e. 4.5x times the average of the previous period. That’s what earned this phase its nickname as the ‘funding heatwave’. That said, the few people who thought it would last forever - or even that funding would stabilise at such high levels - were being foolishly optimistic. Like any period of exponential growth, it eventually had to come to an end.

And indeed, in mid-2022 - again, a few months later than in the US or Europe for instance -, things started to slow down. After such a frenzy, it felt sudden, and many - ourselves included - were quick to dub this new phase the ‘funding winter’. The reality though is that the fall was not nearly as dramatic as the rise had been. As you can clearly see on the graph below, despite the first few months of what felt to some like a free fall, overall the decrease in funding was much more gradual.

And more importantly, it eventually ended. And that’s what this cut of the data shows us. While 2024 numbers were disappointing (-25% YoY compared to 2023) if we stick to a calendar year view, as of March 2025 we have pretty much been in a year-long period of stability again. Something we could be tempted to call a ‘new normal’.

And the good news is: with a minimum of $2b raised over any 12-month period, a maximum of $2.4b, and an average of $2.2 billion, this ‘new normal’ establishes itself about 60% over the last period of pre-heatwave/winter stability. Even if we were to adjust for inflation, at worst the ecosystem would be back to where it started before things got a bit out of control. While maybe disappointing to some, this is not a bad performance considering the current state the world is in, and quite far from the ‘doom and gloom’ stories we sometimes hear…

As always, we’re very keen to hear your feedback on this analysis. Actually, I will try and run something similar on global numbers soon using CB insights’ VC data. It will be slightly different (4-quarterly as opposed to 12-monthly rolling periods as their data is less granular), but still it might help put things into perspective. Stay tuned. In the meanwhile - and especially if you’re new here -, you can find all the underlying data, deal by deal, in our database. And because we love data, and people who love data, there’s a special discount for you. Take care! Max

An interesting analysis.