Same Lineup, Different ranking 🏆

South Africa and Egypt deliver strongest performance in H1 2025

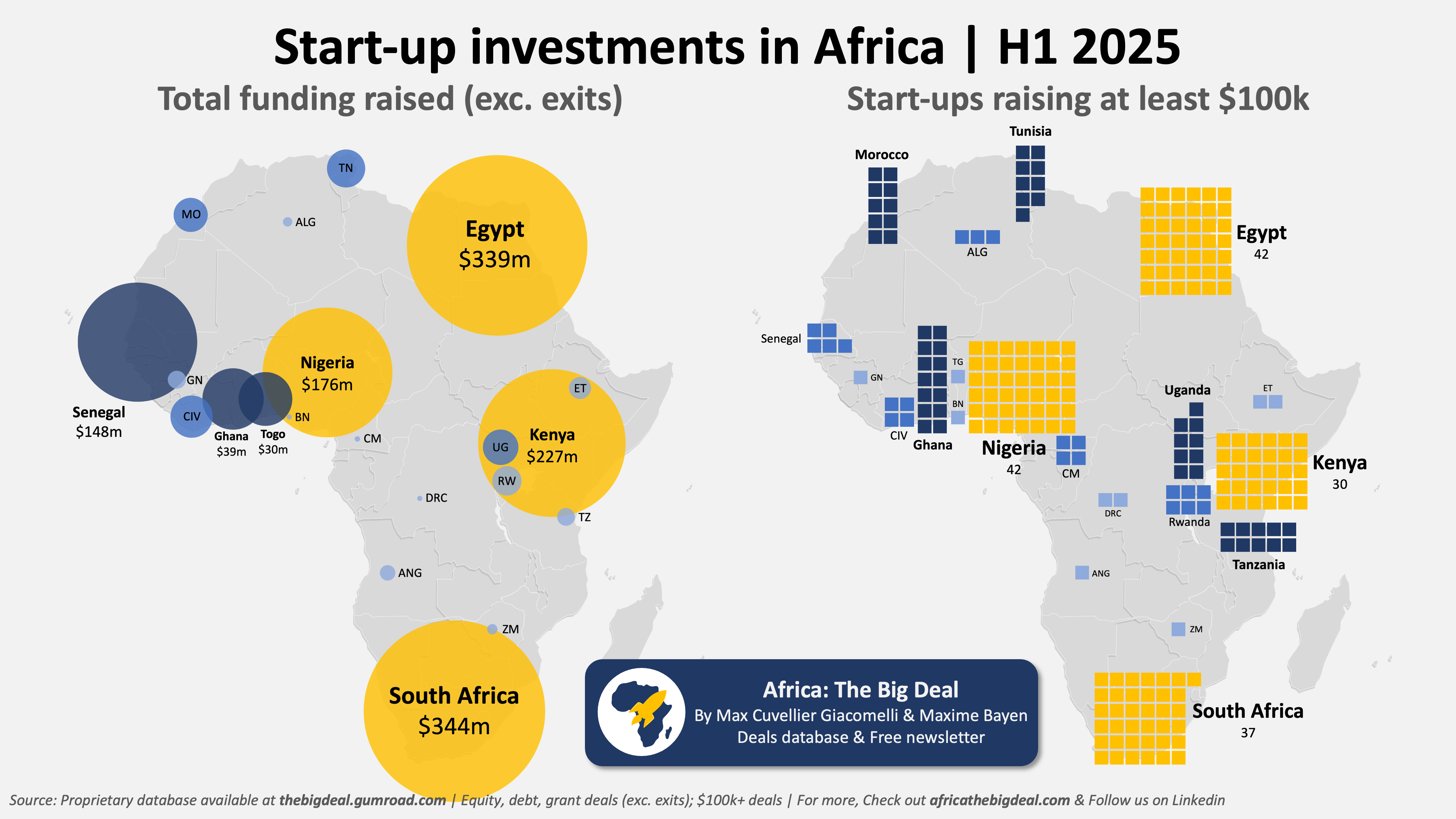

This week we continue to analyse H1 2025 numbers, with a focus on the countries that saw most of the action… As always, the Big Four dominated the rankings with 78% of the total funding raised. Their share of the number of start-ups who raised at least $100k is lower (67%), but reaches 79% if we focus on start-ups who raised at least $1m (84 out of 106). In more detail:

South Africa topped the charts with $344m in H1, its best half-year since H1 2023. While it didn’t claim the largest number of $100k+ deals (37), it boasted the highest number of ventures announcing at least $1m in funding (26). The top3 were hearX (healthtech; $100m), Stitch (fintech; $55m Series B), and Naked (fintech; $38m Series B2)

SuperReturn Middle East returns to Dubai this October! Join 600+ private capital leaders, including 200+ LPs & 200+ GPs, for three days of premier networking and expert insights on venture capital, fundraising, AI, infrastructure, private credit and more. Hear from top firms like KKR, Mubadala, IFC, DFC, Permira & many others…

Egypt was on a similar growth trajectory, claiming almost as much funding as South Africa in H1 ($339m), also its best half-year since H1 2023. A total of 42 ventures raised at least $100k during the period, including 21 who raised $1m or more. The three largest deals (representing half of the total raised) were the $50m bond issued by MNT-Halan’s Tasaheel (fintech), Bokra’s $59m sukuk raise (fintech), and Nawy’s $75m raise ($52m Series A + debt), by far the largest-ever proptech deal on the continent.

In Kenya, the total raised reached $227m; you have to go back as far as H1 2021 to find such a low half-year performance... It ranked #4 in terms of both start-ups raising $100k+ (30) and $1m+ (16). The two largest deals were both in the energy space: Burn Manufacturing with $85m and PowerGen with $55m.

Closing the Big Four ranking is Nigeria with $176m. While the country reigned supreme in the past, especially during the funding heatwave, this is its lowest half-year performance in terms of funding since H2 2020... It did better though in terms of number of ventures raising $100k+ (42, #1 tied with Egypt) and $1m+ (21, #2 tied with Egypt again). LemFi (fintech; $53m Series B), OmniRetail (retail; $20m Series A), and Arnergy (energy, $18m Series B) were the three highest raisers.

Only one week to go! Our Linkedin Live series will be back (with a vengeance!) on July 22, and we look forward to seeing you there. 700 registered & counting...

Interestingly, you have to go back to 2020 to find a similar ranking in terms of funding raised (🇿🇦>🇪🇬>🇰🇪>🇳🇬) before Nigeria (2021, 2022) and then Kenya (2023, 2024) took the lead. But with very large deals expected in Nigeria in particular ($100m for PalmPay?: $300m equity & $1.2b debt for moove??), this could well change by the end of the year…

Beyond the Big Four, Senegal was the only other market to pass the $100m threshold ($148m), with 93% of this amount attributable to Wave Money’s mammoth $137m debt deal. The other three notable $10m+ large deals outside of the Big Four were GoZem (Togo), Zeepay (Ghana) and Djamo (Côte d’Ivoire). Ghana continued to be the market with the highest number of $100k+ deals (14) beyond the Big Four, and good levels of deal activity were also recorded in Morocco, Tunisia, Uganda, and Tanzania.

In 33 markets however, we recorded no $100k+ deals at all in the first half of the year. For 19 of those, we are still to record a single deal over this threshold since we started gathering the data back in 2019…

So, we’ll see you in a week for our Linkedin Live on July 22 of course, but if you’re too impatient and want to dissect the data yourself, you can always refer to our database. If you’re not already subscribed, use this link to claim your reader’s discount. Ci vediamo. Max